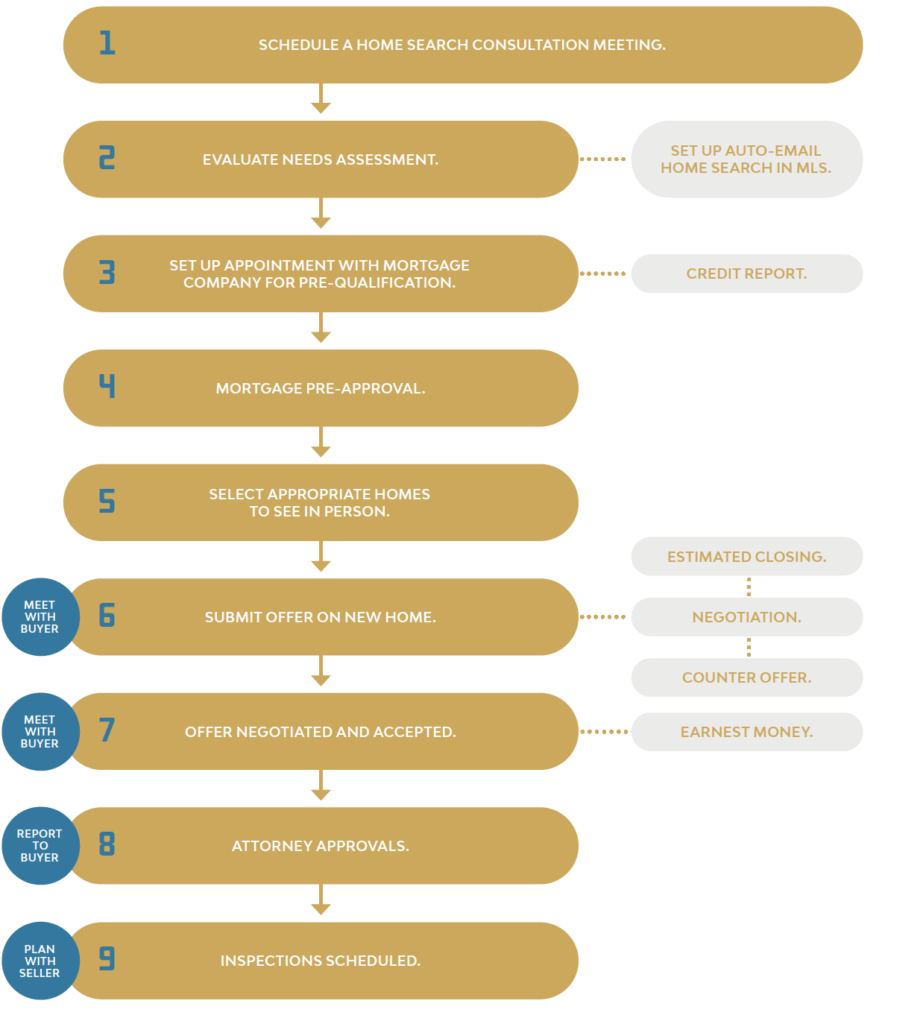

Let Element Realty Services guide you through the entire home buying process.

Element Realty is your partner in residential and commercial real estate. Anyone can participate in the real estate process, but it takes someone like David to make the process less overwhelming, imposing, and frustrating. We are efficient, responsive, and focused. It starts with first getting to know you and your real estate goals. Our range of experience, process, and tools will help you find your way home with a thorough approach that is focused on your goals and preferences.

Meet Your Real,

REal Estate Agent

Both selling and buying your home can be a very daunting task. There is so much to know—from where and how to list, to inspection and mortgage, to making and accepting offers. Taking advantage of reputable resources and covering all bases will save you time, money, and headaches.

This is where David Weitzel steps in. David is a Real Estate Broker, homeowner, and Buffalo investor who understands the nuances of the market, has a long history of construction and sales consulting related to buying, selling, and developing real estate properties, and is an active member of the community.

Benefits of working with David

- Virtual Tours

- Online and social media ads

- Award winning marketing department

- Access to Multiple Listing System (MLS)

- Follow-up on all appointments

- Follow-up on all appointments

- Additional websites

- Open Houses with sales materials

- Personal communication and feedback

- Targeted networking

- Digital Marketing Campaigns

- Extensive construction experience

- Bought, sold, and rehabbed homes

Location, Location, Location.

You might find a dream home, but if it is in an undesirable location, it can be a poor choice! Make sure to consider location questions.

- What is your desired commute time?

- Are senior services or community activities available?

- Is public transportation nearby?

- Do the schools in the neighborhood meet your expectations?

- What is the proximity to grocery stores and shopping malls?

- What schools are nearby?

Make a Wish List

Ask yourself what features are important to you, and what are priorities when looking for your new home.

- How many bedrooms and bathrooms?

- Do you want a garage? Is it attached?

- How much land do you want?

- Do you want a fixer upper, or a new home?

- What about a finished basement?

- What style(s) of home(s) do you love?

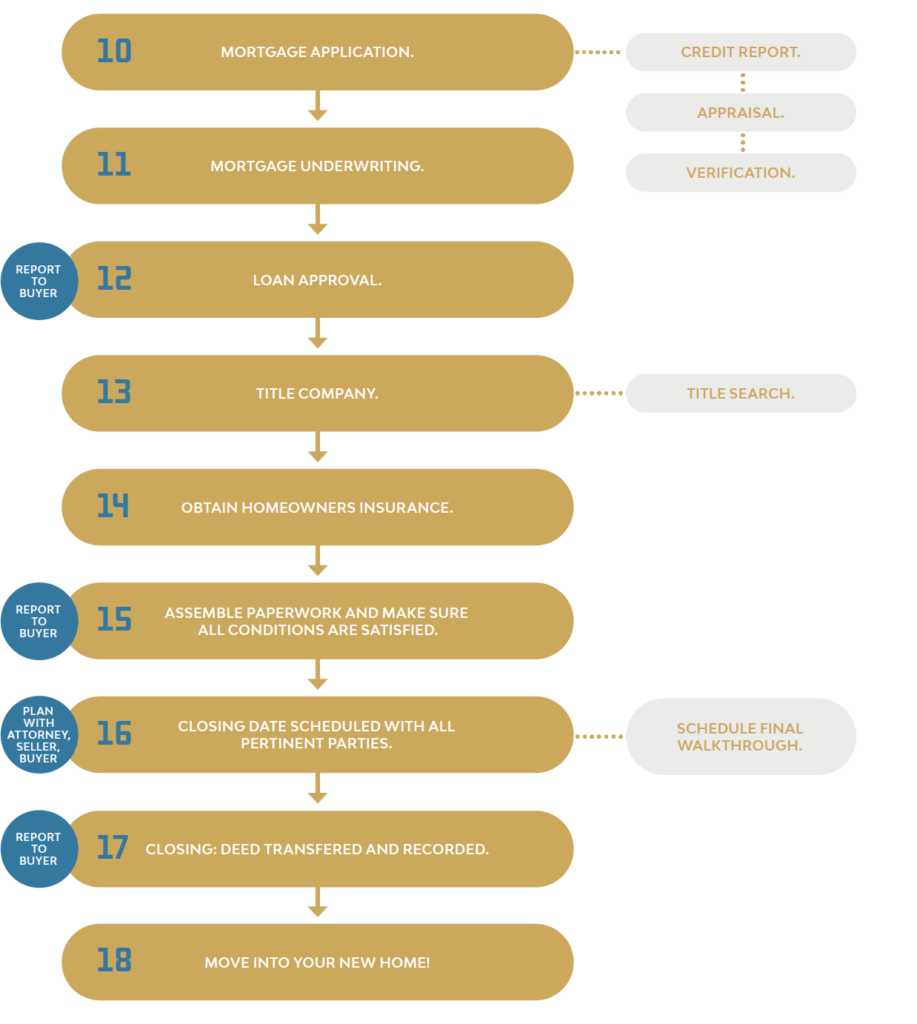

Get Pre-Approved for a mortgage.

Make sure you get pre-approved for a mortgage before looking at homes. The amount you qualify for might be more or less than you anticipated. This shows that you’re serious, and strengthens your position when making an offer.

Do your Homework and be organized.

With access to the web, there’s so much information available to you on current markets, trends, and pricing. Keep track of what you find, and take photos and notes of the home visits to help narrow your search to match your wish list.

Be prepared to make an offer.

Know what is in a purchase contract so you can anticipate what you’re getting into when it is time to make an offer. Refer to your wish list, notes, and budget notes as you make pricing and offer decisions.

Relax!

Buying a new home is a life-changing event. Don’t allow it to become overwhelming. Take time to unwind and level your thoughts. Don’t make any impulsive decisions, and keep things into perspective. With research, diligence, and patience, you’ll find a great fit!

Application

☐ Check for application fee.

Property Information

If you have an existing contract:

☐ Purchase agreement.

☐ Copy of legal description and MLS sheet.

If you are selling your current home:

☐ Copy of listing contract.

If you have sold your current home:

☐ Copy of settlement statement (HUD-1).

Debts

(Including all loans, Credit Cards, etc.)

☐ Names, addresses, account numbers, and balances of each.

☐ Monthly payment amount of each.

If you have credit report anomolies:

(Such as late payments, charge-offs, collections, judgements, and liens, or credit inquiries in the last 90 days)

☐ Explanation of each.

If you have filed for bankruptcy within the last 7 years:

☐ Copy of bankruptcy papers.

VA Loans

☐ Copy of DD Form 214, Report of Separation.

Indentification

☐ Photo ID

☐ Proof of Social Security

☐ Residence addresses for the past two years.

☐ If applicable, a copy of your divorce decree.

☐ If you are not a citizen, a copy of the front and back of your green card.

Income and Assets

☐ Pay stubs for the last 30 days.

☐ Names and addresses of each employer for the last two years.

☐ W2s for the last two years.

☐ Statements for each bank, and investment accounts the last three months.

☐ Estimated value of all personal property (furniture, electronics, vehicles, boats, ATVs, etc.)

If you have any large deposits in your accounts:

☐ Explain the source of the deposit.

If your large deposit was a gift:

☐ Signed gif letter (lender can supply).

☐ Copy of gift check.

☐ Copy of deposit receipt.

If you own more than 25% of a business:

☐ Corporate or partnership tax returns.

If you are self-employed:

☐ Tax returns for the last three years (with schedules).

☐ Year-to-date Profit and Loss Statement prepared by an accountant.

If you own rental properties:

☐ Tax returns for the last two years and current rental agreements.

If you are retired:

☐ Pension award letter.

If you receive social security:

☐ Social Security award letter.

If you are counting child support as income:

☐ Copy of divorce settlement.

☐ Copy of twelve months of canceled child support checks.

Abstract of Title

A complete historical summary of the records relating to the public ownership of a particular piece of land.

Adjustable Rate Mortgage (ARM)

A mortgage in which the interest rate changes over time, based on an index.

Affidavit

A statement the buyer or seller may be asked to sign at the closing, attesting to certain information.

Annual Percentage Rate (APR)

The cost credit as an annual rate of a mortgage. It must be calculated by using a formula set by federal law and disclosed to the borrower to aid in comparing different credit plans.

Appraisal

A professional’s estimate and opinion of the market value of a property.

Appreciation

An increase in the value of a property due to changes in market conditions, home improvements, or other factors.

Assessed Value

The value placed on a home by municipal assessors for the purposes of determining property taxes.

Balloon Loans

Loans in which regular monthly payments are followed by a lump sum payment of the total outstanding balance.

Bridge Loan

A short-term mortgage made until a longer-term loan can be made; it’s sometimes used when a person needs money to build or purchase a home before the present one has been sold.

Cash Reserve

A requirement of some lenders that buyers have a certain amount of cash remaining after closing.

Closing

The final steps in the transfer of property ownership. Closing typically occurs at a formal meeting between the buyer, seller, settlement agent, and the buyer’s and seller’s agents. At the closing, the buyer signs the mortgage and mortgage note, the seller receives payment for the property, and the buyer and/or seller pay closing costs. Once accomplished, title is transferred from the seller to the buyer. Also referred to as Settlement.

Closing Costs

The total costs of completing the transfer of ownership of the property, other than the purchase price.

Contingency

A clause in the purchase contract that describes certain conditions that must be met before the contract is binding.

Conventional Mortgage

Any mortgage that is not insured or guaranteed by the federal government.

Debt-to-Income Ratio

A ratio that measures total debt burden. It is calculate by dividing gross monthly debt repayments, including mortgages, by gross monthly income.

Disclosures

Usually refers to providing information about a property for sale, especially as it represents actual or potential defects or problems. “Full disclosure” usually refers to the responsibility of the seller to voluntarily provide all known information about the property.

Earnest Money

A deposit of money given by the buyer to bind a purchase offer and which is held in escrow until the sale is closed.

Engineer Inspection

A physical inspection of the major systems of a house by a licensed professional as a contingency of the sale. The fee is paid by the buyer. An engineer’s inspection is recommended but not required.

Equity

The value of the property, less the loan balance and any outstanding liens or other debts against the property.

Escrow

Funds held by a neutral third party (the escrow agent) until certain conditions of a contract are met and the funds can be paid out.

Fannie Mae

The Federal National Mortgage Association, a major national investor in home loans. A private corporation created by Congress to support the market and increase the availability and affordability of home loans for low-, moderate-, and middle-income Americans.

FHA/HUD Insured Mortgages

A mortgage insured by the Federal Housing Administration of the US Department of Housing and Urban Development and made by an approved lender or servicer in accordance with the FHA/HUD regulations.

First Mortgage

The mortgage that has first claim in the event of default.

Fixed-Rate Mortgage

A type of mortgage loan in which the interest rate does not change during the entire term of the loan.

Freddie Mac

The Federal Home Loan Mortgage Corporation, a major national investor in home loans. A private corporation created by Congress to support the secondary mortgage market and increase the availability and affordability of home loans for low-, moderate-, and middle-income Americans.

Lein

A legal claim against a property the must be paid when the property is sold.

Loan-To-Value-Ratio (LTV)

The percent of the appraised value of a property (or the sales price of that property, if it is lower) that may be loaned.

Lock-In

A written guarantee that the buyer will receive a specified interest rate, provided that the loan “closes” within a set period of time.

Market Value

The amount a willing buyer would pay a willing seller for a home. An appraised value is an estimate of the current fair market value.

Mortgage Broker

A company or individual that matches borrowers with lenders for a fee.

Mortgage Insurance

Insurance purchased by the buyer to protect the lender in the event of default. Typically purchased for loans with less than 20 percent down payment.

Points

A dollar amount paid to a lender if it is necessary to reduce the interest rate (not commonly done).

Radon

A colorless, odorless radioactive gas that results from the natural decay of uranium in the earth.

Savings and Loan Association (S&L)

Depository institutions that specialize in originating, servicing, and holding mortgage loans.

Savings Bank

A financial institution organized to hold individual depositors funds in interest-bearing accounts—and to make long-term investments such as home mortgage loans.

Survey of Property

Surveys are conducted by a licensed surveyor and are usually required by the lender in order to confirm that the property boundaries and features such as buildings, improvements, and easements are as detailed in the legal description of the property in the deed.

Title

A legal document establishing the right of ownership. Also known as the Deed.

Title Insurance

An insurance policy that guarantees the accuracy of the title search and protects against potential errors. Most lenders require the buyer to purchase a title insurance policy protecting the lender against loss in the event of a title defect.

Zoning

Zoning laws are local laws that are established to control and guide the uses of land within a particular zone. An important use of zoning law is to separate residential land use from areas of non-residential use that would affect the quality of life in a community. Zoning ordinances may dictate a variety of factors, such as type of structure, setbacks, lot sizes, and uses of buildings.

Helpful Contacts

Gas & Electric

NYSEG

800-572-1111

National Grid

716-832-2400

National Fuel

716-686-6123

Phone

AT&T

716-875-1500

Sprint

716-875-4444

T-Mobile

716-877-9012

Verizon

716-840-8688

TV & Internet

Spectrum

866-874-2389

Dish Network

855-650-4270

Verizon Fios

716-423-2180

Direct TV

888-325-6631

Water

Erie County Water Authority

716-849-8444

Buffalo Water

716-847-1065

Refuse

Big Trash Removal

716-262-8420

AAA Trash Be Gone

716-602-9611

Other

General Help

Dial 311

Poison Control

800-222-1222

NYS DMV

518-473-5595

www.dmv.ny.gov

City of Buffalo

www.buffalony.gov

Post Office

www.usps.com

Buffalo Water

716-847-1065